Since the turn of the past decade, smaller lenders have taken the credit industry by storm – making giant, liquidity-filled strides all over the world. These are essentially small banks and non-banking financial companies (NBFCs), who have capitalized on the limitless potential of technology to offer credit to sectors like agriculture, education and Small and Medium Enterprises (SMEs), where large banks haven’t managed to penetrate that well. At the same time, umpteen NBFCs haven’t managed to gather a lot of capital to fund their credit offerings to modern customers. To bridge this gap, co-lending has come to the rescue.

Co-Lending: What is it?

In essence an arrangement between cash rich banks and non-deposit holding financial institutions (NBFCs) and housing finance companies (HFCs), co-lending has become extremely popular between many players in the market. While the NBFCs would do the grunt work of loan origination and paperwork, banks would offer their liquidity strength to finance a majority of the loan. In co-lending, both parties share the risks and rewards throughout the loan lifecycle.

NBFCs have always benefited from their ability to pierce smaller, harder-to-reach geographical areas through the use of modern loan origination softwares and banking practices. This led to excellent growth rates, but with limited liquidity, there is only so far that NBFCs can get ahead in the market. Banks on the other hand, have a bigger clientele, bigger wads of cash and bigger fee structures. Co-lending is a give-and-take model by which NBFCs can improve their liquidity, profitability and client base, while banks can advantage from the market outreach, loan origination and servicing acumen of NBFCs.

How does a Co-Lending Agreement Work?

NBFCs and banks are obliged to enter a tripartite agreement with customers and play the co-lending game. The process is fairly simple, but has to be executed to the T to ensure a streamlined arrangement. Here are the 3 steps:

1. First the NBFC performs loan origination activities through co-lending softwares and checks on the prospective client, after which it recommends him/her to the partner bank with the relevant documentation.

2. The bank independently does requirement analysis and risk assessment of the client and vets him/her if found credit worthy.

3. The lending parties enter into a three-way agreement with the client. The bank and NBFC pool their funds into an escrow account from which the loan shall be disbursed. Although both lenders will maintain the client’s accounts, they must share information and collaborate to generate a unified statement of accounts for the borrower for easier repayments.

Features of the Co-Lending Model

Ever since the Reserve Bank of India (RBI) announced the Co-Lending financial model, banks and NBFCs have embraced the ‘co-origination’ process that entails a bevy of features targeted at mutually profiting both parties:

- Banks and NBFCs will usually take on an 80%-20% exposure limit in offering the loan to clients, with NBFCs mandated to maintain at least 20% of the funding throughout the loan term.

- The portion of loan given out by the NBFC cannot be funded by a partner bank. Loan provisioning will be done independently by the NBFC and the bank.

- Both parties’ funds must be collected and allocated in their agreed ratio at the time of funding and at the time of repayment collections, in such a way that neither party uses the funds that belong to the other.

- Both parties can charge their own interest rates, and the customer must pay the ‘blended’ interest rate.

- Loan origination will be done by the NBFC, with a risk assessment done by both NBFC and the partner bank.

- The repayment scheme for co-lending loans will follow the NACH mandate through ‘Standing Instruction’ debits from the customer account.

- Sometimes, NBFCs can also tie up with multiple banks for a distributed capital deployment; for example, the NBFC puts 25% stake, Bank A lends 40% and Bank B gives 35% of the loan amount.

Blended Interest Rate

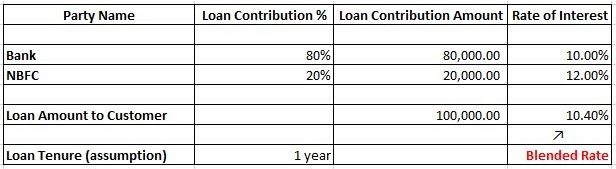

As per the rules laid down by the RBI, co-lending warrants that the NBFC and bank together offer a blended or a weighted-average interest rate to their customer. Here’s simple illustration of how it works:

Say NBFC A wants to offer a co-lending, loan product of ₹100,000 to Mr. Vaibhav. NBFC A has a co-lending agreement with Union B bank. The bank is ready to shell out ₹80,000 at an interest rate of 10% per annum and NBFC A pitches in ₹20,000 at 12% per annum. The weighted average interest rate that the customer gets is derived using the below formula:

Blended Rate = [(₹80,000 x 10%)+(₹20,000 x 12%)]/(₹80,000 + ₹20,000) = 10.40%

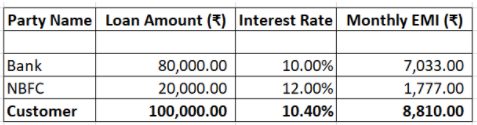

Repayment Schedule

There are 3 types of repayment schedules created at the time of loan agreement – one each for the NBFC, the bank and the customer. Using the above example, let’s explore how this works:

- The NBFC’s interest rate is 12% and will levy a monthly EMI of ₹1,777 every month for 1 year, with a total accumulated interest amount of ₹1,324.

- Union B bank will take ₹7,033 monthly and will gather a total interest of ₹4,399.

- The customer instead will follow the blended interest rate of 10.4% and pay a monthly EMI of ₹8,810.

NBFCs Role in Co-Lending

Using the power of technology, NBFCs have powered ahead in the lending industry even in the tiniest of geographical areas. Due to this outreach and loan management softwares, they can quickly and efficiently onboard hordes of customers under the co-lending approach. NBFCs have to provide a pre-agreed volume of loan originations in a set time period to the partner bank under any form of agreement.

The onus is on these NBF companies to explain to customers about the difference between their own product offerings and products under the co-lending category. Document sharing, customer service and grievance redressals also form part of the responsibility checklist of NBFCs.

How NBFCs Will Benefit by Co-Lending

Albeit in its nascent stages, co-lending can make some serious breakthroughs in the credit industry. NBFCs are touted to grab most of the spoils in the process – here’s how:

- No more funding constraints for NBFCs while targeting high net worth individual (HNWI) clients as their exposure is limited to about one-fifth.

- The framework from the central bank is very transparent – this helps NBFCs steer clear of any regulatory pressure.

- NBFCs can watch and understand best practices of loan origination and risk assessments from large banks, and implement some of these practices through co-lending softwares like CloudBankin to improve operational efficiency.

- Since the NBFC and bank have to create a business continuity blueprint at the commencement of a co-lending partnership, the NBFC can offer unperturbed service to its customers.

- An opportunity for NBFCs to improve their Assets Under Management (AUM), with the backing of a big-name bank.

Present Challenges in Co-Lending

Since its introduction in the market, co-lending has not gained the kind of traction as was expected with both NBFCs and banks. Some of these challenges are:

- Common credit approval standards

- Integration to a common IT infrastructure, which could potentially streamline many origination and disbursement processes.

- Constantly fluctuating lending policies with banks and NBFCs.

- Since co-lending is a new concept, NBFCs and banks alike could be faced with accounting challenges which can easily be tackled using co-lending softwares.

- Integration of credit and risk management systems (both digital and non-digital) of the two parties.

- Processing fees that banks and NBFCs charge are quite different, and this has led to many challenges in collaborations.

Since it is a very new concept, co-lending is targeted only towards the Priority Sectors. For it to gain traction, global markets need to stabilize and growth needs to start ticking up.

Digital Drive in Co-Lending

As is the case with most NBFCs, going digital for all aspects of lending has become the norm. Some digital initiatives include automated onboarding of customers, document capture, online credit risk assessment using the customer’s credit history, EMI monitoring and regulatory compliance updates for both banks and NBFCs.

These days, time is of the essence. By incorporating a scalable IT infrastructure, co-lending partners can reduce loan origination and disbursement turnaround time from a few days to just a few minutes.

Future Roadmap of Co-Lending

There is little doubt that co-lending will prove to become a holy grail of business for NBFCs in the coming years. Big banks like the SBI are making inroads to partner with tech-rich NBFCs to implement this concept. The rules of this game are still being formed and it remains to be seen if scenarios wherein multiple banks or NBFCs can get together in an arrangement. In which case, what would be the credit risk requirement of each NBFC? But it’s only a matter of time before co-lending spreads its arms across mainstream sectors and becomes a success mantra for other economies.

Related Post

Impact of Budget 2021 on Banks & NBFCs

As COVID-19 wreaked havoc across industries in India in 2020,

Conclusion: Significance of Uniform Credit Reporting For Financial Institutions

Significance of Each Segment in the Uniform Credit Reporting Format

5 Use Cases to drive ROI through BNPL as a Lender

The pandemic-induced economy has expanded the credit market in India